Part of a series on FinGoal’s opportunity tags.

FinGoal is excited to announce that the next few months will see the launch of our opportunity tagging product on the Insights API. FinGoal opportunities are designed specifically for FIs to match end users with relevant FI products or services that the user is likely to benefit from. Using our opportunity tagging API, FIs can run targeted marketing campaigns designed to prompt end users with the right opportunity, at the right time.

Today, we’re going to start with our HELOC opportunity tag. In particular, I’d like to showcase how personalizing outreach with FinGoal’s opportunity and user tags helps create marketing that’s truly helpful for the end user.

Personalization has become one of those dime-a-dozen, technocorporatese words that pervades the workplace. Ostensibly, all personalization means is that a platform or application makes display decisions based on user data. That generates quite a range of user experiences. There’s very simple personalization (Welcome back, ${user.nickname}!). Then there’s the more involved, yet commonplace, personalization (”You watch a lot of videos about snakes. Could we interest you in some more general reptile-focused content?”).

What has personalization meant in tech? I propose a definition: “Personalization in technology refers to any dynamic user experience that changes as a result of user data inputs.” It means the decisions that users have made in the past influence the present, and it’s responsible for even the most sophisticated recommendation algorithms.

${your_fi}?Let’s face it. Other apps have it easier than financial apps, because they’re designed to be open for a long time. In fact, the length of time over which the app is open is often a key success metric for certain companies. Let’s make an example out of a generic video streaming platform. A user watches videos on that platform. That platform collects data on the videos the user watches. These videos are associated with other videos also on the platform. These other videos are promoted to the user, on the platform. The user watches these videos…

You already know the rest of the pattern. But notice that every component of the process— user’s actions, outcomes, recommendations—are all handled in the platform itself. This is personalization made simple. All of the required data for the recommendation engine is collected by the platform, to be used by the same platform. Nothing’s leaving the house.

That’s not the case for FIs. No matter how good your online banking experience is, your end user isn’t going to use it for hours—in fact, if your users are spending hours in your online banking experience, you might have a problem. How can you personalize when you don’t have the user data to spur an informed recommendations?

This is where transaction data steps in. Your FI may not have the same digital information that the modern technology platforms do, but you do have a wealth of transaction data. If anything, this data shows your user’s preferences better than any click ever could—these aren’t measly clicks, this is your end-user’s hard earned cash!

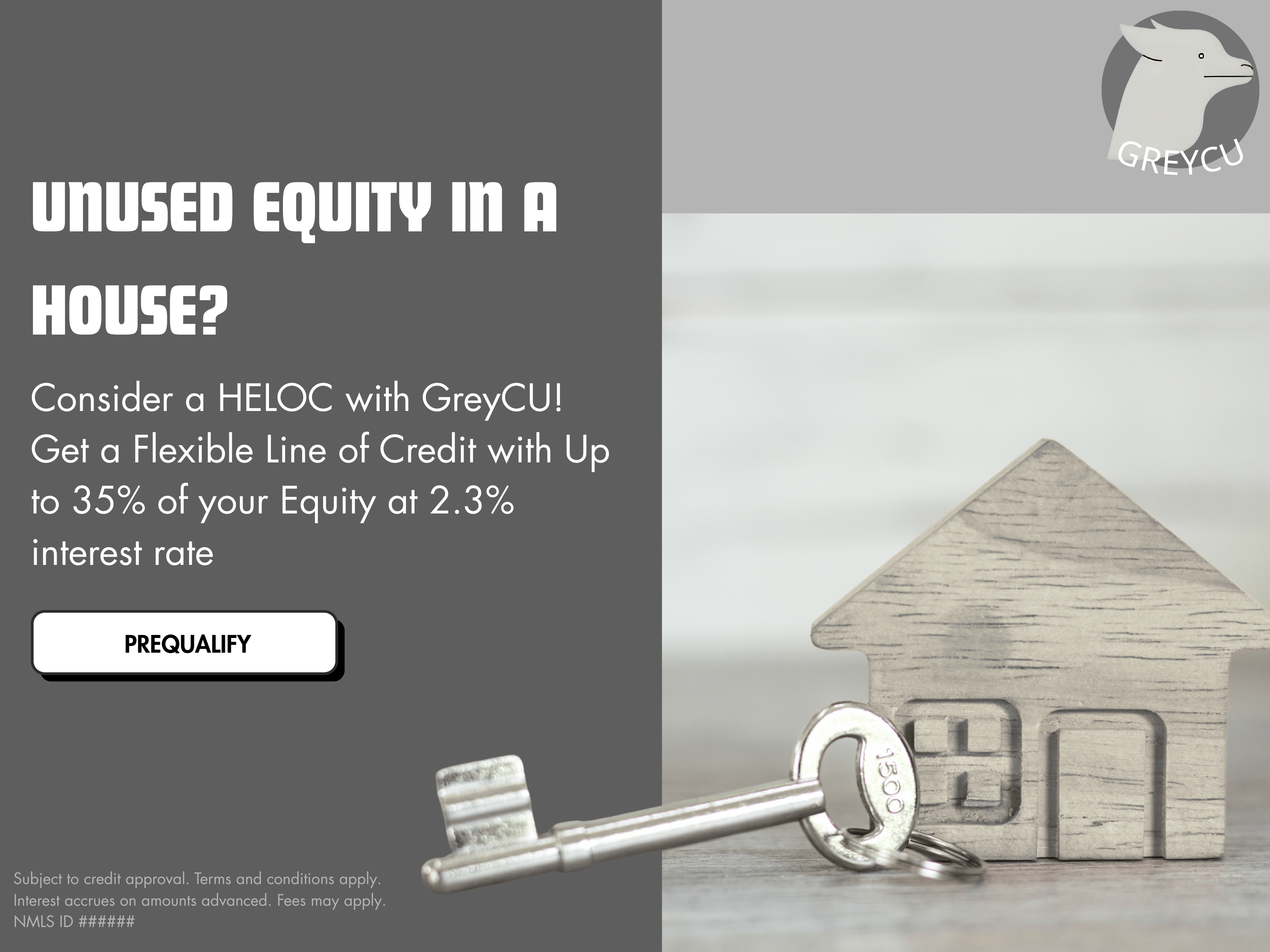

FinGoal is purpose-built to plug insights from this transaction data back into your marketing software, allowing you to make smarter decisions based on behavioral data. Now, I promised a HELOC example. I had better deliver.

Say your FI has a fantastic HELOC product, but isn’t quite sure how to market it.

There’s the old spray-and-pray strategy, that might work well enough. You can look through all of the individuals who bank with your FI and identify the ones who have not yet received a HELOC from you (pretty simple filtration, really). Finding only those users without an active HELOC, you target them with a call to action to open one.

There’s some obvious drawbacks to this strategy. The most glaring is that you will send the marketing material to individuals who don’t even own a home. In such cases, your prompt was at best irrelevant and at worst irritating. It’s not the end of the world, but it’s also not ideal.

If you’re a small community FI, your users might wonder why you don’t seem to know them any better than the big, impersonal, national FIs do. Your end-users might ask, “Shouldn’t my FI know whether or not I have a mortgage?” With FinGoal’s Insights API, you can.

Our API’s user tags feature finds users who have payments to mortgages in their transaction history. Surfacing this mortgage tag, we can update your FI’s marketing automation tool with a list of who has a mortgage, and who don’t have a HELOC.

.png)

Now we can run what I might call an “under-personalized” campaign, as demonstrated above. It’s definitely better targeted than the old spray-and-pray, but it still has some weaknesses. In particular, it doesn’t do much to let the end user know why you’re prompting them with this product now. Sure, the user has a mortgage, but it’s possible that they have for a while. They might ask, “Why does my FI think I need this line of credit right now?”

I don’t know about you, but when I get a marketing email from my bank with an initiative that’s only vaguely relevant to me, I always assume it’s an initiative to promote a product at my bank and not a product or service that’s actually relevant to me. This isn’t an ideal user experience, since it makes me feel like I’m serving my FI, rather than my FI serving me.

Good news! There are a number of strategies that FinGoal recommends to better-target a HELOC offer, with an call to action that’s relevant to the user. The Insights API offers hundreds of user tags that can be used to better personalize opportunity tags. For this article, I’ll choose just one such user tag, the unexpected home expense.

For this personalization, we assume we’re only looking at individuals who FinGoal has has determine to hold a mortgage. Say one such individual has recently had one or more unexpectedly large, non-recurring home expenses in their transactions—a highway-robbery-sized plumber bill or an HVAC expense in the middle of summer. These transactions might suggest that something bad, or at least surprising, is happening with the user’s home. A lot of us have been here: A rogue wind whips a tree-branch through our kitchen window; a terrible hailstorm totals our roof (welcome to Colorado); we’ve got a broken water heater (If you know…). Moments like this are financially stressful times for people.

.png)

By using the HELOC opportunity tag in concert with the unexpected home expense user tag, we can send targeted, personalized, and well-timed marketing for the HELOC product to the relevant users. With Insights API’s unexpected home expense user tag, we flag only those users who have these unforeseen costs within the past sixty days, so we know that the HELOC alert is timely. The user isn’t left wondering, “Why now?”

This kind of nuance does more than to shallowly personalize the offer. It actually makes it relevant to the person who receives it. Rather than looking like a product the FI has an initiative to promote, a HELOC marketed in this way looks like a product that the FI genuinely believes is right for the end-user at this precise moment. The call to action is much more immediate, giving an end-user a much stronger reason to really consider the product.

When I log into my bank app, I don’t want to see a list of card linked offers with the FI’s business partners. I don’t want to see the products and services that the FI wants to sell me. I want to see offers, products, and services that are relevant to me specifically, which could make a palpable difference in my financial picture and serve me better.

With FinGoal’s opportunity tags, your FI can serve your customers the way they want to be served. That, perhaps, leads to a better definition of personalization, and one that stretches it beyond a buzzword: “Personalization in financial technology should refer to any dynamic user experience that changes as a result of user data inputs, and results in a better financial position for the user.”

.png)